30x in 15 Months

Job Loss in AI Revenue

In the previous post I argued the disruption is just beginning, and that it would move beyond software into every industry that sells human expertise. Here I put numbers on it. The leading indicator is Anthropic’s revenue. The lagging indicator is jobs.

Anthropic’s annualised revenue grew from $87 million in January 2024 to $44 billion in late April 2026. That is roughly 30x in fifteen months. There is no precedent for it in enterprise software history. The question this post asks is whether anyone is going to lose their job over it, and the answer is yes.

The argument runs in three parts. First, that frontier AI revenue is large enough, growing fast enough, and concentrated enough in substitutive use cases that it must be displacing labor at scale. Second, that the displacement is not visible in the headline unemployment rate because of how the labor market absorbs structural shocks, through hiring freezes, wage stagnation, lower participation, and underemployment, rather than through layoffs. Third, that this is global. Some of the displacement is happening to outsourced knowledge work in countries the US labor statistics do not see.

30x in fifteen months

Anthropic publishes its annualised revenue run rate every few months. ARR is current monthly revenue multiplied by twelve. It is not the same as full-year revenue collected, but it is the standard metric for tracking trajectory in cloud businesses. When you see “$30B run rate” in headlines, it means current monthly revenue is about $2.5B.

OpenAI is also growing fast, about 3x year-over-year, but Anthropic’s curve is steeper. Combined, the two largest frontier AI labs reported around $69B in run rate by May 2026. Google does not disclose its AI-specific revenue cleanly, but Google Cloud is at a $70B+ run rate growing 48% year-over-year, and Google has stated that its enterprise AI solutions grew nearly 800% year-over-year in Q1 2026. The true number for total frontier AI revenue today is somewhere between $90B and $130B. I will use the conservative $69B for the rest of this post.

Where do the curves go?

Three scenarios about what happens next, all starting from $69B in May 2026 (combined Anthropic + OpenAI run rate).

Naive extrapolation assumes current growth rates hold. I use 10x per year as the working figure: this roughly matches Anthropic's standalone pace over the last fifteen months and sits above the combined Anthropic + OpenAI rate, which is closer to 5x per year. If anything, 10x is generous to the case that growth slows quickly.

At 10x per year, the curve crosses 100% of global GDP by August 2029. Even cutting that rate in half, at 5x per year, the curve still crosses 100% of global GDP by December 2030. Both are reductios: the world is not large enough to fund either case. They tell you, immediately, that current growth rates cannot continue. The question is what shape the slowdown takes.

Growth decay assumes the current 20% month-over-month growth bleeds off as the labs exhaust easy demand. At a moderate decay rate, the combined run rate reaches $400 to $600B by 2028, roughly 0.3 to 0.5% of global GDP.

Logistic saturation assumes an S-curve with a natural ceiling. Set the ceiling at $500B (roughly the size of the largest software companies today) and the curve passes through $300B by 2028 and approaches the cap by 2030.

All three scenarios reach the hundreds of billions of dollars in combined run rate by 2028, differing mainly in pace. Let’s explore what that could mean for labor markets.

From dollars to people

Revenue is a dollar amount. Job loss is a count of people. The bridge between the two is where most pieces about AI and jobs fall down.

The bridge is what I will call the capture multiplier: the ratio of labor income substituted to dollars of AI revenue collected. If a firm pays Anthropic $10,000 and that lets it forgo a $200,000 contractor, the multiplier on that transaction is 20x.

In January 2026, Ryan Stevens at Ramp published Payrolls to Prompts, the first paper to identify the multiplier from firm-level spending data. Ramp is an expense management platform, so the dataset covers thousands of companies and their actual spending on freelancer marketplaces (Upwork, Fiverr, Toptal) and AI model providers (OpenAI, Anthropic) from late 2021 to late 2025. Stevens uses ChatGPT's October 2022 launch as a natural experiment, comparing how firms that were heavily exposed to freelancer spend before ChatGPT shifted their budgets afterward.

The headline finding: for firms most exposed to AI shocks, every $1 reduction in labor marketplace spend corresponds to a $0.03 increase in AI model provider spend. That is a capture multiplier of roughly 33x. For the middle exposure quartile (firms with 50 to 75% of pre-ChatGPT spend on labor marketplaces), the ratio is $1 for $0.30, or 3.3x. Stevens writes that “the true magnitude most likely lies somewhere between these two quartiles,” and explicitly notes the estimate is conservative because it does not capture in-house infrastructure costs or increases in engineering headcount needed to deploy AI.

One important caveat. Stevens measures dollars of marketplace spend substituted per dollar of AI spend, which is not the same as labor income destroyed per AI dollar. Marketplace spend includes platform fees (10 to 20% on Upwork), freelancer overhead, and contractor margins, so only 60 to 80% of that spend was ever labor income. And displaced freelancers do not all go to zero income; some shift to other work, take in-house roles, or move down-market. The appropriate discount for translating channel substitution into labor income destruction is roughly 0.5 to 0.7.

Applying that discount to Stevens, the labor capture multiplier is in the range of 2x to 23x, with a central estimate around 12x to 15x. I will use 12x as the default. This is more conservative than Stevens' raw findings would suggest, but it correctly accounts for the fact that not every dollar of marketplace spend is permanently destroyed labor income.

Three things matter about this. First, the multiplier is high because AI does not compete on price the way human labor does. Anthropic's API costs cents per task; the labor it substitutes was paid in tens of thousands of dollars. AI captures a small fraction of the value it creates: the dollars Anthropic charges are an order of magnitude smaller than the labor income they substitute. This is the deflation paradox.

Second, not all AI revenue is substituting labor. Some is additive (companies adopting Claude on top of their existing teams to do things they could not previously afford). Some is substitutive. The fraction that is substitutive is the substitution share, and we have data on it. The Anthropic Economic Index classifies every Claude conversation as either augmentation (human in the loop) or automation (the model doing the task on its own). Across five reports between January 2025 and April 2026, the Claude.ai automation share has bounced between 41% and 49%. On the API (where enterprise traffic lives and where substitution actually happens) automation is around 75%, and the share classified as "directive automation" rose from 27% in December 2024 to 39% by February 2026. Anthropic's own characterisation: "the underlying trend is still toward greater automation."

Third, Anthropic's own November 2025 productivity paper corroborates Stevens from a different angle. Across 100,000 real Claude conversations, the median task would have cost $54 in human labor and was completed 81% faster with AI. Controlled academic studies in narrower settings find smaller per-task time savings (14 to 56%), which probably better reflects real-world conditions once you account for users refining outputs and checking quality. The truth is somewhere in that range. At any point in the range, the labor cost saved per task dwarfs the AI cost incurred, which is the mechanism behind the multiplier Stevens measures.

To translate revenue into job-equivalents:

jobs displaced = (AI revenue × substitution share × capture multiplier) ÷ average wage

How many jobs

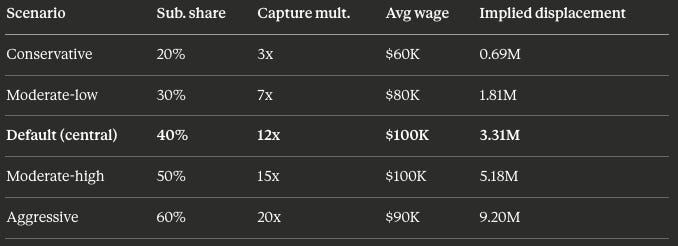

Plug conservative defaults into the formula: combined frontier AI revenue $69B, substitution share 40%, capture multiplier 12x, average wage $100K.

($69B × 0.4 × 12) ÷ $100K ≈ 3.3 million job-equivalents

Five scenarios, varying the parameters:

The aggressive case anchors at Stevens’ upper-quartile estimate discounted to labor income (33x × 0.6 ≈ 20x). The conservative case (3x) sits at Stevens’ middle-quartile estimate discounted similarly. Both endpoints are now empirically grounded.

Push every parameter to the lower end of what is empirically defensible and the model still produces several hundred thousand job-equivalents. The default settings produce 3.3 million. No scenario in this table is small.

Two reactions are reasonable. The first is “that is high, there have not been 3 million layoffs.” The second is “that explains some things.” Both have something to them.

Why 3.3 million is invisible

US headline unemployment is around 4.3%, and the unemployment rate has not moved much in two years. If 3.3 million jobs had been destroyed, you would expect to see it. You do not. So what is going on?

Four things at once.

Employment growth below trend. When a company decides AI can do work that an entry-level analyst used to do, it does not fire its current analysts. It just does not hire next year’s. The labor that “would have been there” never materialises.

The clearest signature of this in the data is the deceleration in monthly job gains. According to BLS Employment Situation releases, nonfarm payroll employment averaged monthly gains of 166,000 in 2024, slowing to just 15,000 per month in 2025. The September 2025 preliminary benchmark revision further reduced total nonfarm employment as of March 2025 by 911,000, indicating that even the 2024 figure had been overstated. As of April 2026, total nonfarm payroll employment had shown little net change over the prior 12 months.

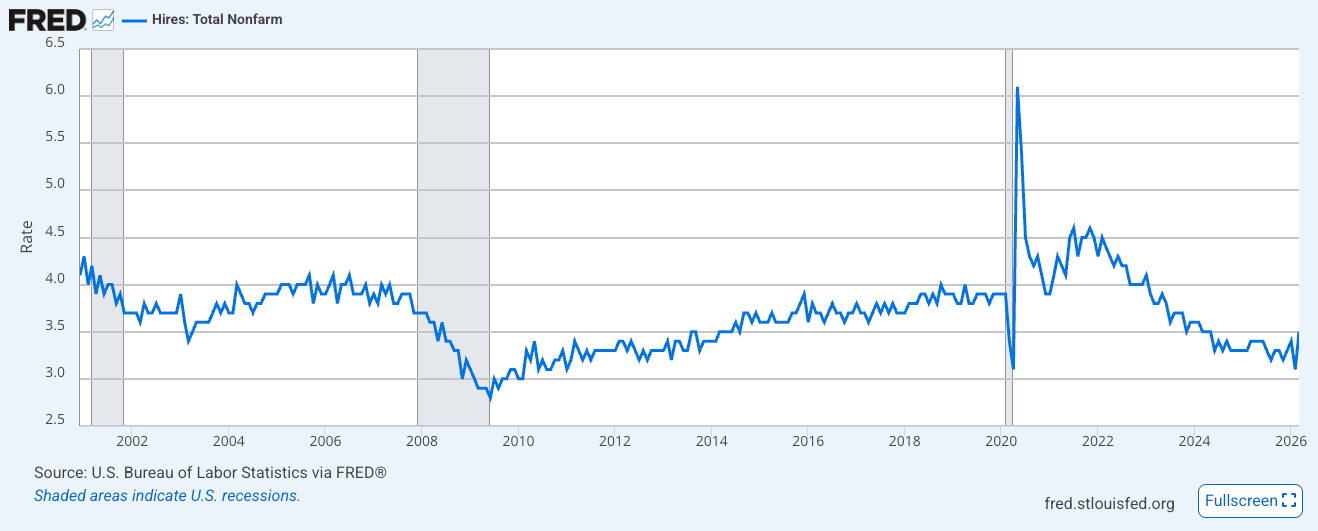

The JOLTS hires rate corroborates the same story. It stood at 3.5% in March 2026, below pre-pandemic norms, which is consistent with broad demand suppression. Firms are not opening new positions when existing staff leave. The signal is in employment growth flatlining, not in any single month’s hires count.

Most of this is the post-pandemic over-hiring correction working through the system, not AI. Tech and finance over-hired in 2021 to 2022 and have been unwinding since. The question is what fraction of the persistent slowdown reflects AI specifically. The Indeed Hiring Lab notes that tech-adjacent sectors are showing the sharpest weakness: information sector job openings down 33% year-over-year, IT infrastructure roles 30% below pre-pandemic levels, which is exactly what the AI-substitution thesis predicts. There is no clean way to decompose the AI-attributable share, but it credibly accounts for 1 to 2 million missing positions in the persistent gap.

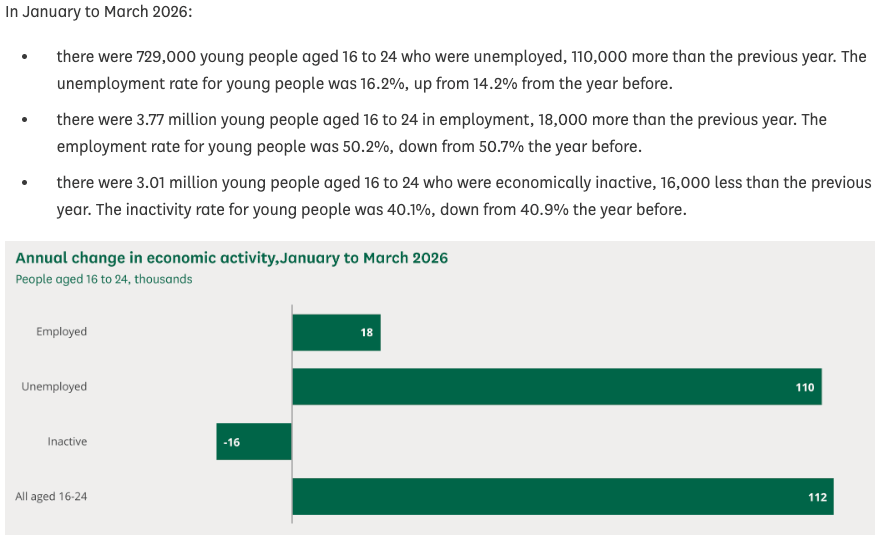

Entry pathway collapse. Senior people do not get replaced. The bottom rungs of the ladder do. UK youth unemployment has surged over the last eighteen months while overall unemployment has stayed flat. This is not because young people got worse at working. It is because the jobs young people used to enter the workforce through (research analyst, junior copywriter, paralegal, customer support) are the jobs being substituted first.

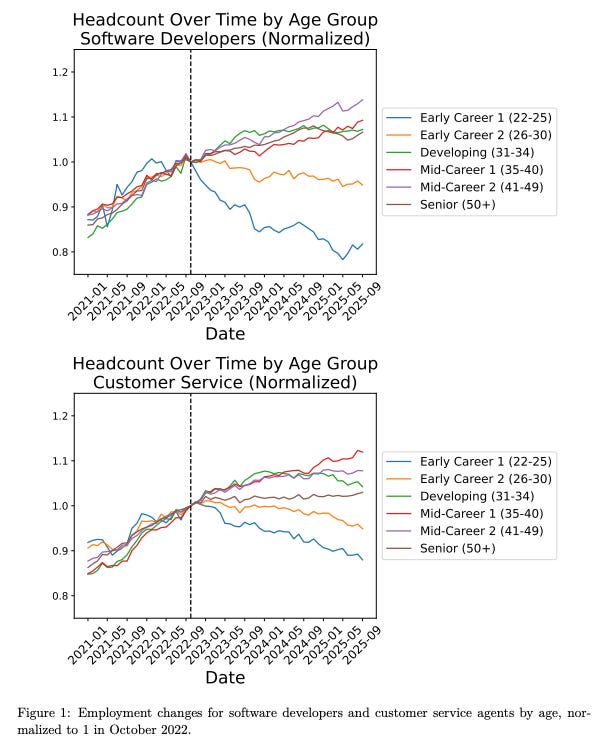

Brynjolfsson, Chandar, and Chen's Canaries in the Coal Mine finds the same pattern in US payroll data: employment for early-career workers in highly AI-exposed occupations declines sharply relative to older workers, whereas employment for more experienced workers is broadly stable.

The missing hires above already include these young workers; entry pathway collapse just shows where in the labor market those missing hires are concentrated. It's the most visible symptom of the squeeze.

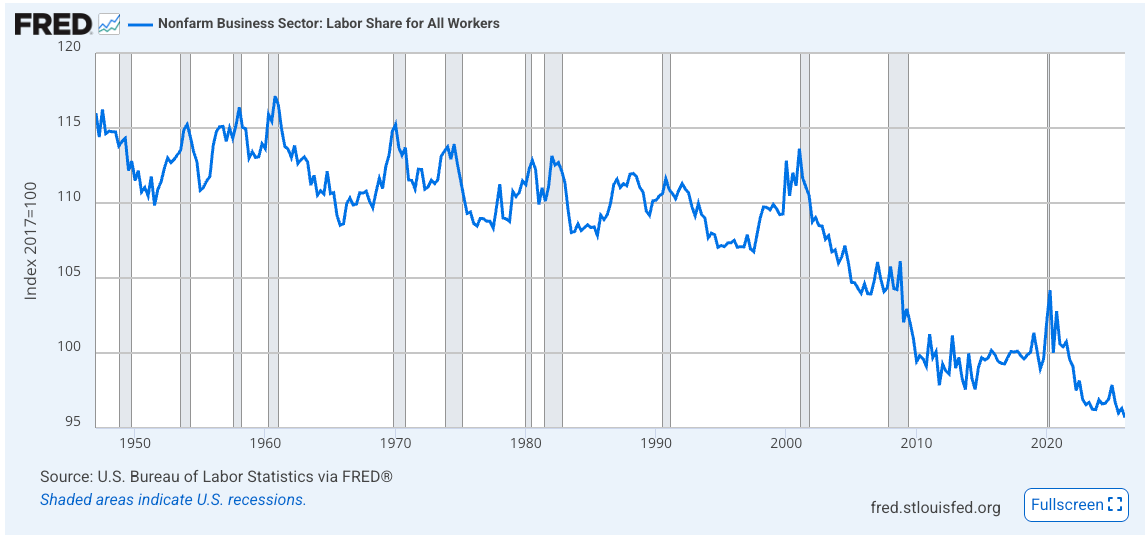

Wage stagnation. When AI makes labor cheaper to substitute, wages for the substitutable jobs stop rising. Workers who keep their jobs see flat or shrinking real income. This is not a layoff and it is not unemployment. It is the same labor income captured at a discount. The labor share of US GDP has fallen by about 0.8 percentage points since 2023, against a trend that was modestly rising. Labor share has been declining for decades, so the entire 0.8pp is not completely AI-attributable. If half of the recent acceleration is AI-related, that is 0.4pp on a $30T economy, or $120B of annualised labor income captured at a discount. Divided by an average wage of $100K or 1.2 million job-equivalents.

Underemployment composition shift. The headline figure (42.5% of recent graduates working in jobs that do not require a degree as of Q4 2025, 41.5% as of Q1 2026) sounds dramatic, but recent graduate underemployment has historically ranged between 40% and 50% for decades. What has changed is the composition: the share of underemployed graduates working in "good non-college jobs" (paying more than $45,000) fell from 47% to 34% between 2009 and the present, with most of the decline since 2023. The AI-attributable share here: 100,000 to 300,000 job-equivalents.

Some of the displacement is not in the US at all. A meaningful share of the work that frontier AI is substituting was outsourced to India, the Philippines, and other countries in the first place. A US enterprise paying Anthropic to deploy Claude for customer support or developer productivity may be deploying it against teams in Bengaluru or Manila. The dollars flow through California but the impact lands somewhere else and the US labor statistics do not see it.

Add the US-side buckets at central estimates: 1.0M + 1.2M + 0.2M = 2.4 million job-equivalents, with offshore additional. This sits in the same neighborhood as the 3.3M from the substitution model we saw above.

The 3.3 million figure is an estimate of the labor-equivalents already displaced from where the economy would otherwise be, distributed across vacancies that never opened, wages that never rose, pathways that never produced their next cohort, and offshore teams whose contracts are being thinned.

The displacement that isn’t local

The model in this post estimates US displacement, but the substitution is not contained by the geography of where the revenue is collected. A US enterprise paying Anthropic to deploy Claude for “developer productivity” may be deploying it against engineering teams in Bengaluru, Manila, or Warsaw. The revenue goes to California, but the impact lands in countries that built their economies on knowledge-work outsourcing.

The Philippines BPO sector employed 1.82 million workers in 2024, projected to reach 2.5 million by 2028 and generates around 8% of national GDP, with $38 billion in export revenue in 2024 growing to roughly $59 billion in 2028. India's IT and BPM sector employed around 5.8 million workers and generated $283 billion in revenue in FY25, contributing roughly 10% of GDP. Together that is over 7.5 million workers across the two countries supporting an industry north of $320 billion per year. The IMF working paper on the Philippines published in February 2025 found that 89% of the BPO workforce faces high risk of automation, with 14% of the total Philippine workforce at risk of direct replacement by AI.

Anthropic’s own data confirms where the substitution is happening. The Anthropic Economic Index India Country Brief (February 2026) reports India as the second-largest market for Claude.ai usage globally at 5.8% of total use, with software tasks accounting for 45.2% of Indian Claude usage versus 36% globally. Web development usage in India runs 1.9 times the global average. India is using Claude disproportionately for exactly the kinds of tasks that BPO and IT-services workers in India have been paid to do.

So far the headline numbers look fine. The Philippines added around 135,000 BPO jobs in 2024, and the Philippine trade association IBPAP projects an additional 1.1 million jobs by 2028 against a 2022 baseline. The Indian IT-BPM sector continues to grow revenue. But entry-level hiring is being squeezed: a 2025 EY analysis estimates entry-level IT roles in India have declined by 20 to 25% due to automation, with NASSCOM reporting workforce growth in the Indian tech sector slowed to 2.3% in FY26. Revenue continues to grow while headcount growth flattens, which is the firm-level signature of productivity substitution.

Based on the above, I would esimate 30 to 40% of the global displacement implied by frontier AI revenue is probably happening outside the US. Philippine BPO at 1.9 million workers with 89% high-risk exposure, plus Indian IT-BPM at 5.8 million with maybe 60 to 70% high-risk exposure, gives a base of roughly 6 million offshore workers in the immediate firing line. Even modest substitution rates against that base produce 1 to 2 million displaced job-equivalents.

This strengthens the thesis. Some of the substitution is felt abroad and the aggregate US labor market doesn’t see it.

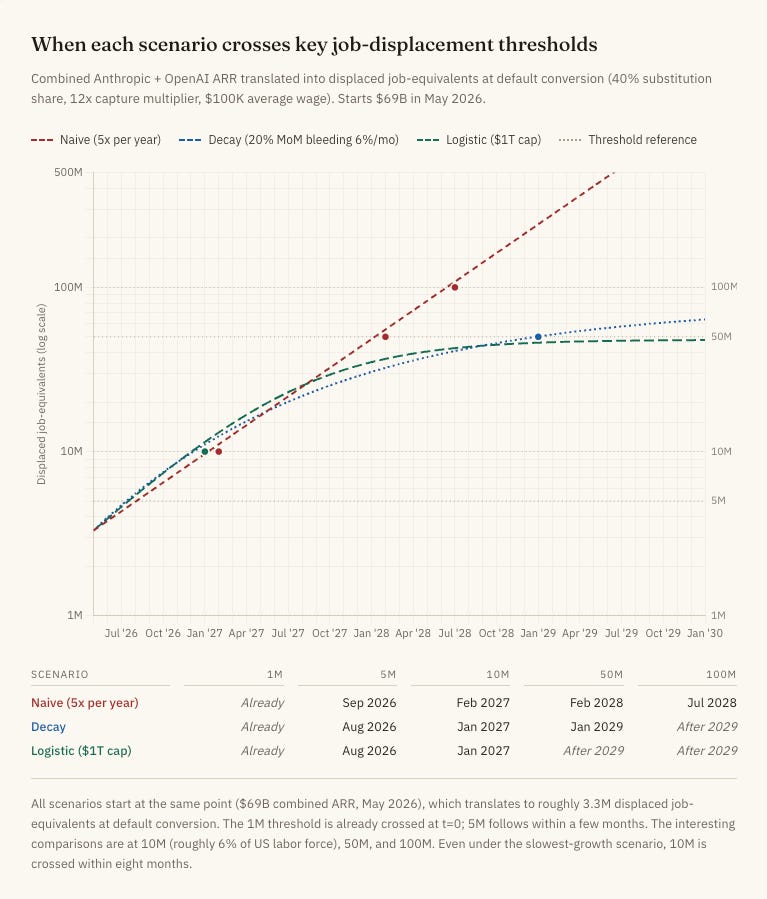

The threshold crossings that matter

Three scenarios for combined Anthropic + OpenAI ARR growth from $69B in May 2026 through end of 2028, with default conversion assumptions. When does each scenario cross specific job-displacement thresholds?

Even under the slowest-growth scenario, 10 million job-equivalents are crossed by early 2027 under default assumptions. That is roughly 6% of the US labor force. Push every parameter to its conservative end (20% substitution, 3x multiplier, $60K wage) and the timing pushes out by a year or two, but the crossings still happen inside the five-year window.

The point is not the specific date. It is that the displacement is already large under any plausible assumption, already showing up in the data for anyone looking at the right metrics, and growing fast enough that the absorption mechanisms will not hold indefinitely.

Where this leaves us

This post started from one number: $44B in annualised revenue, grown from $87M in fifteen months. That number is a leading indicator for something else, the displacement of labor. Every dollar of frontier AI revenue corresponds to some quantity of labor income that has been redirected from human workers to AI providers and their compute infrastructure.

The substitution model takes that revenue and a set of parameters and produces an estimate of how many job-equivalents are implicated. Under settings I think are conservative defaults, the estimate today is roughly 3.3 million job-equivalents, with the actual displacement split between the US and the countries that historically did outsourced knowledge work. The absorption buckets (missing hires, wage stagnation, smaller contributions from labor force exits and underemployment composition) sum to a number in the same neighborhood. The model and the data are pointing the same direction.

What happens next depends on whether frontier AI revenue continues to grow at anything close to its current pace. The slowest scenarios cross 10 million job-equivalents by early 2027. The fastest cross 100 million by mid-2028.

A leaving note. The right frame here is to protect people, not jobs. A job that AI does better should be done by AI. A person whose labor income disappears because of that substitution should not be left to absorb the loss alone.

The productivity gains AI unlocks are real and worth wanting. But the dollars from displacement currently flow to AI providers and their compute infrastructure rather than to the workers whose labor was substituted, and that distribution gap is what needs to be addressed by policy. Dario Amodei, Anthropic’s CEO, has proposed a token tax: a small fraction of revenue from every AI model call routed to redistribution. The specifics matter less than the principle. As the capture multiplier compounds and the displacement scales, some fraction of that captured value has to make its way back to the people whose labor it substituted.